|

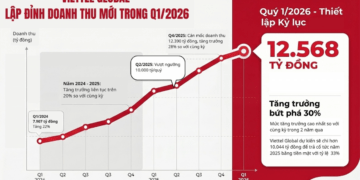

In Q1 2026, MSN posted net profit after tax before minority interest (NPAT Pre-MI) of VND1.97 trillion ($75.77 million), doubling on-year. Consumer-retail earnings before interest and taxes (EBIT) rose to $94.62 million, up 23.6 per cent on-year, reflecting broad-based growth across the platform.

Q2 2026 preliminary momentum indicates MSN is on track to grow NPAT Pre-MI by approximately 60 per cent on-year.

WinCommerce (WCM) – the company operating the WinMart/WinMart+/WiN chains – delivered NPAT Pre-MI of $7.85 million in Q1 2026, up 3.5 times on-year, equivalent to a 1.8 per cent margin. The result is driven by higher store traffic, disciplined network expansion and operating leverage.

WCM recorded a net addition of 225 new store openings for Q1 2026, bringing the total store count to 4,817 nationwide. Notably, 100 per cent of new store openings surpassed store‑earnings before interest, taxes, depreciation and amortisation breakeven level within the quarter.

Like-for-like (LFL) growth across all formats was primarily driven by higher store traffic (bill count) as modern trade penetration accelerates. Among them, minimarts delivered LFL growth of 11.8 per cent on-year in Q1 2026, up from 8.6 per cent in Q1 2025.

Supermarkets delivered LFL growth of 19.9 per cent on-year for Q1 2026, up from 6.1 per cent in Q1 2025, supported by renovations that lifted store traffic. Supermarkets also achieved EBIT-positive with 3.5 per cent margin, up 386 per cent on-year points (bps) on-year. As of March 2026, 60 supermarkets have been renovated, with the remainder on track for completion by year-end.

Masan Consumer’s Q1 2026 revenue reached $325.77 million, up 13.1 per cent on-year, while NPAT Pre-MI reached $69.23 million, up 11.5 per cent on-year.

Retail Supreme demonstrated clear improvements across key execution metrics as March 2026. First, active selling outlets reached approximately 500,000, up 2.3 times compared to before Retail Supreme. Second, stock keeping unit per order reached 5.5 (up 17 per cent) while approximately 57,000 outlets now carry around six or more categories, up 2 times. Third, approximately 50,000 outlets are implementing MCH’s in-store execution standards, up 1.8 times.

Masan Consumer’s gross margin was stable at 46.7 per cent on-year.

|

Masan MEATLife (MML) delivered revenue of $95.38 million in Q1 2026, up 19.8 per cent on-year, with NPAT Pre-MI of $5.65 million, up 27.2 per cent on-year. EBIT grew on-year to a 7.4 per cent margin, up 450 bps on-year, as both fresh and processed meat benefited from improved economies of scale and higher porker utilisation. Total MML sales at WCM grew 30.2 per cent on-year.

Phuc Long Heritage posted net revenue of $21.88 million in Q1 2026, up 34 per cent on-year. The EBITDA margin reached 20.8 per cent while NPAT Pre-MI grew 1.6 times on-year to a 10.3 per cent net margin, up 260 bps on-year. Growth was driven by delivery scaling and stronger in-store productivity gains, with LFL average daily sales in standard-format stores reaching $1,011.54, up 21.2 per cent on-year.

Masan High-Tech Materials (MSR) delivered a record quarterly NPAT of $20.65 million in Q1 2026, compared with a $8.54 million loss in Q1 2025, supported by stronger commodity pricing, improved operating performance, and lower net interest expenses.

Net revenue reached $115 million, up 114.9 per cent on-year, led by APT revenue of $94.23 million, up 3.2 times on-year. APT averaged $1,865/mtu in Q1 2026 and reached $3,150/mtu as of March 31, 2026, compared with MSR’s revised 2026 budget assumption of approximately $1,200/mtu. In the event current price levels are sustained for the rest of the year, MSR expects to achieve materially better financial results.

Throughput is expected to recover from Q2 2026 and ramp further in Q3 2026 following the amendment of the 28-million-tonne mining licence, with full-year ore processed projected to exceed FY2025 levels.

MSR is expected to generate stronger operating cash flow and accelerate deleveraging, with revised guidance indicating net-debt-to-EBITDA declining from 3.5 times in Q1 2026 to 1.7 times by year-end.

Assuming APT prices average above $1,500/mtu, MSR targets net-debt-to-EBITDA of 0.1 times by end-2027, and conservatively net cash position by end-2028, which would create room for lower interest expenses, higher earnings quality, and potential dividend payments in the upcoming years.

Masan has announced plans to migrate MSR to the HSX mainboard, aiming to enhance value recognition, broaden the shareholder base, improve liquidity, and support strategic investor engagement.

MSN’s profit share of Techcombank in Q1 2026 was $50.77 million, up by 11.8 per cent on-year.

Building on a record Q1 2026, MSN’s revenue and NPAT Pre-MI are estimated at $1.98 billion and $176.92 million in the first half of 2026, up 38 per cent and 76 per cent on-year, respectively.

|

Masan posts steady gains as Vietnam targets stronger retail growth

Vietnam’s push for stronger retail growth by 2030 is being matched by improving performance in the country’s major consumer groups. |

|

Masan Consumer lifts foreign ownership limit to 100 per cent

On March 18, the State Securities Commission announced that it had received Masan Consumer Corporation’s application to double its foreign ownership limit to 100 per cent. |

|

Masan High-Tech Materials plans HSX listing

Masan High-Tech Materials has released documents for its 2026 AGM, slated to take place in Hanoi on April 16. |

{kind=link}