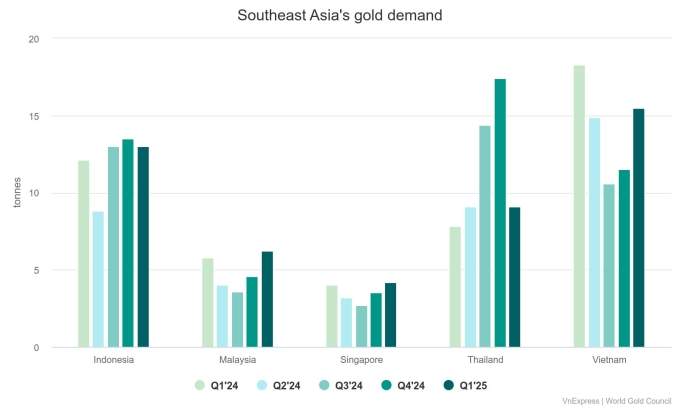

Thailand’s gold demand rose 17% year-on-year in the first quarter, the biggest growth in five countries studied in Southeast Asia.

The country recorded a consumer demand of 9.1 tons, according to a recent report by the World Gold Council.

Singapore, Malaysia and Indonesia saw growth between 5% and 8%, while Vietnam bucked the trend with a 15% decline.

For gold bar and coin, Thailand’s demand jumped 25% year-on-year to 7.4 tons, signifying a strong tendency of local investors in purchasing a safe-haven asset amid global economic uncertainties.

“It’s been a bumpy start to the year for global markets as trade turmoil, unpredictable U.S. policy announcements, sustained geopolitical tensions and a return of recessionary fears have created a highly uncertain environment for investors,” said Louise Street, senior markets analyst at the World Gold Council.

In this context, investment demand for gold has paved the way for the highest level of first-quarter demand since 2016, she added.

Global gold demand, including over-the-counter trades, reached 1,206 tonnes in the first quarter, a 1% year-on-year increase, despite gold prices soaring past US$3,000 per ounce.

{kind=link}